New data emerges for construction risk insurance

Having a gut feeling that something is not right is one thing but having clear sight of the statistics to prove that is quite another. Liz Booth spoke to Stephan Lämmle, of the International Association of Engineering Insurers, and Tim Chapman, of the London Engineering Group, about how new statistics are set to transform the conversation for the construction insurance sector

Keeping the conversation open between insureds, brokers and insurers is crucial but so is giving risk managers transparency about the state of the insurance market.

New statistics being released by the International Association of Engineering Insurers (IMIA) are designed to do just that for the construction sector, providing everyone in the chain with a clear view of claims, premiums and loss ratios.

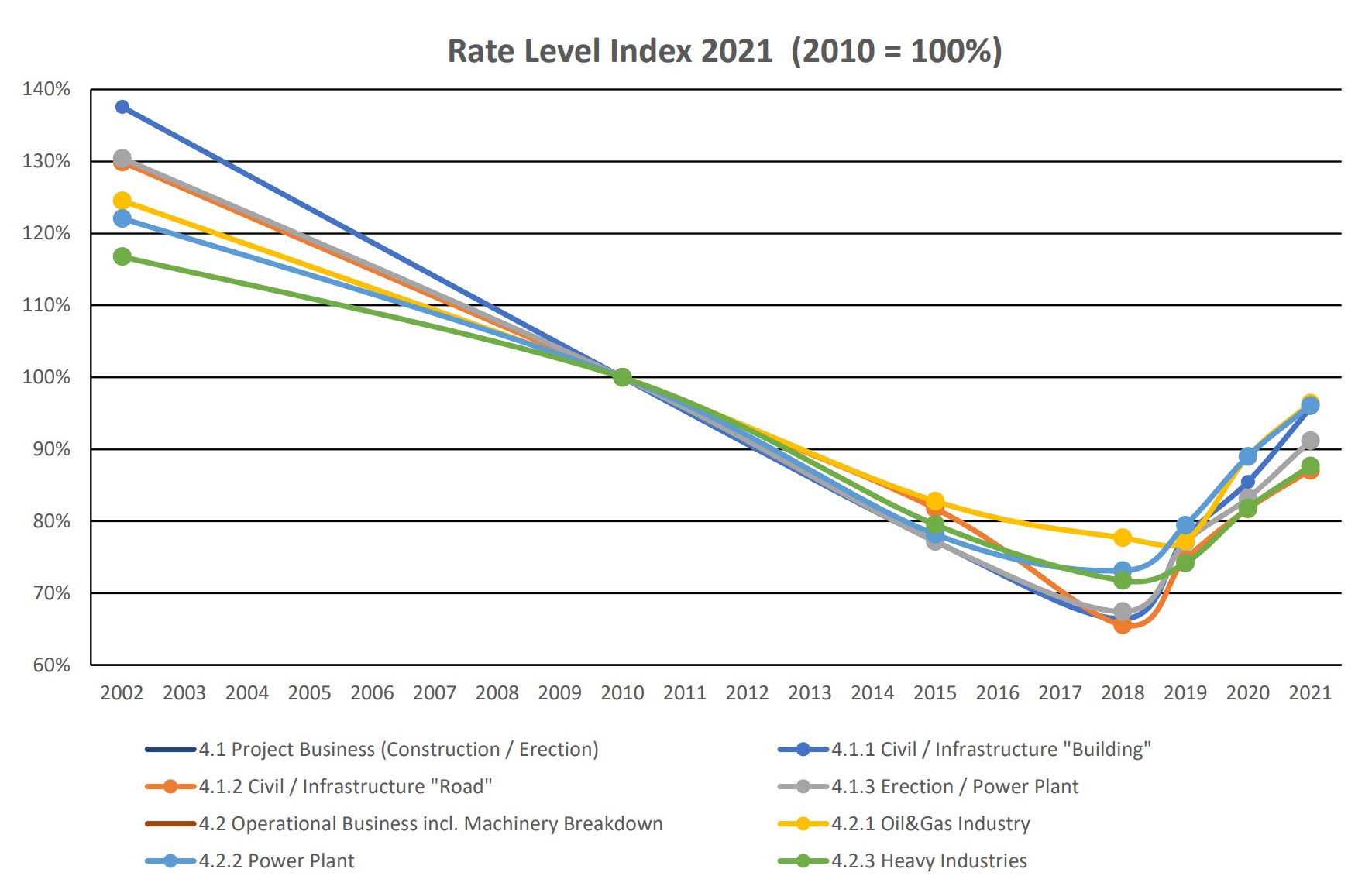

Chairman Stephan Lämmle highlighted that the latest figures show a clear uptick in premium values, however, the chart (below) also clearly shows the ‘hockey stick’-shaped V and the fact that premiums are still less than half of the value from 2002.

That message was reiterated by Tim Chapman, chairman of the London Engineering Group (LEG), who said: “We know our market is cyclical and we have been through a long soft cycle, bottoming out in 2018/2019.”

But he stressed: “Rates were below a sustainable level at that point and as a result we lost several markets. Since then, rates have increased but they are not back to historic levels as demonstrated by the IMIA statistics.”

This message echoes that from experts talking at Commercial Risk’s Construction Risk Management webinar in December. At that event, a group of experts discussed the state of the market and the challenges facing insureds in a hard market: Michael Earp, architects and engineers practice leader, Aon; Mark Peterson, managing director, professional services, Aon; Ariana Dalie, director, risk, Dragados Canada; and Amanda Burnell, senior underwriter, vice-president, Liberty Specialty Markets.

Across the Commercial Risk webinar and also at the LEG and IMIA conferences held late last year, the message was the same: insurers recognise rates have risen sharply in percentage terms, but it needs to be asked whether in real terms (absolute figures) the premium is sufficient to create a sustainable marketplace. Similar topics were debated with brokers during the October LEG Conference panel discussion, titled: ‘Is the London Construction Insurance Market Sustainable?’

A few weeks on, Lämmle added: “It would be alright if rates were low and losses were equally low, but it is no good if rates are falling but losses are staying the same – or worse, growing.”

Both Lämmle and Chapman stressed that communication lies at the heart of the issue. “In my experience,” said Lämmle, “risk managers don’t want surprises. The rate increases are hard, but it is not knowing what to expect that makes their lives much tougher.”

Chapman added: “The difference now is that, thanks to the IMIA stats, we can see the trend clearly and that is what we need to be communicating to insurers, insureds and the brokers. It is no longer a gut feeling but a reality which we can see clearly.”

He also explained the unique and long-tail nature of construction projects: “We are often underwriting long-tail projects of five or even ten years’ duration, and consequently it can be many years before a claim materialises. It is difficult to price a risk now to accurately reflect the environment faced in ten years’ time. For instance, insurers are paying out on claims arising from emerging risks such as climate change, secondary perils, claims inflation and new technology. These risks have been insufficiently taken into account in the models and are therefore often underpriced.”

An example of that, he said, was flash flooding in the Middle East. The frequency and severity of the floods has increased dramatically in recent years, attributed to climate change, but had not been foreseen when policies were underwritten several years ago.

“We have been seeing rapid increases in secondary perils (such as from climate change),” said Chapman, “and those were not written into the terms and conditions five years ago.”

In the past few months, supply chain bottlenecks have become an issue for the sector and the pair expect an increase in delay-in-start up claims. The supply chain issue is also impacting the cost of replacement materials, potentially resulting in increased costs for the insurers.

So far, they agree the pandemic itself has not changed the market dynamic too much – although projects slowed to begin with, most picked up again fairly quickly and construction in major cities has continued unabated.

However, new risks are emerging. For example, said Lämmle, technology is resulting in new ways of working as well as new materials. He pointed to 3D printing, which is set to change the industry. However, Lämmle warned: “That and increasing use of prefabrication means that if you make one error in one place, you could have 1,000 errors to put right, representing a new series loss exposure.”

It will take time for these impacts to be visible to insurers, brokers or insureds, said Chapman. “The statistics are historical and give us a really good picture of what has happened. But they do not tell us what will happen in the future,” he explained.

Instead, he said the LEG Group is being asked for technical training by its members, who want to make sure, for example, that their wordings are correct for the emerging environment and also that they keep abreast of emerging risks.

However, as Lämmle pointed out, the new statistics have a real purpose in helping the market understand the context in which they will move forward. “Before we had these statistics, we were flying blind,” he said, “and now we have transparency.”

Both men believe that the new facts and figures will help the relationship between insureds, brokers and insurers improve, because there will be greater transparency and better communication.

- On 18-19 May 2022, Commercial Risk will host its third Construction Risk Management Conference. For more information about attending, speaking or partnering please visit: https://www.commercialriskonline.com/events/construction-2022